Coincidentally, I've been reading Naomi Klein's "Shock Doctrine", which outlines the steps taken by the Chicago School of Economists to undermine and replace the economic systems of Chile, Argentina, Poland, and Russia with radical Milton Friedman Free-for-all Market economies. The step of allowing Lehman's to fail, and the completely predictable ensuing chaos that would entail, giving the chance for the Treasury Secretary to step in and claim monarchical powers (Nouriel Roubini was the 1'st to recognize this, when in response to the plan he remarked, "This is not A Monarchy"... hah! it is now, buddy) is only the first step in a tried and true formula for a financial coup d'etat:

In the 1'st daze of the Bush administration, he asked for the privatization of Social Security, needing approximately $1-2 trillion to do so:

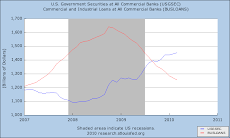

$700 billion...proposed b/o pkg

$438 BD (budget Deficit)

$200 Fanny Mae;Freddy Mac

$160 Rebate checks

$85 AIG

$29 BS bailout...sounds cheap now, eh?

-------------------

$1.6 trillion

and it ain't over yet....oh, and nowhere in those numbers are the cost of our wars included, nor the increase in interest payments that an additional couple of trillion dollars'll add to the deficit.

The exact amount of the bailout requested as a boondoggle to Wall St by infusing it with the avalanche of cash from the "privatization" of Social Security.

Just as he financed his war via the tax receipts of the Wall ST. Robber Barons, he's repaying that favor now, since the ruse to infuse them with American Workers' savings failed.

But that's just my opinion....I could be wrong.

But even to a clueless economic observer like me, the inevitability of this "crisis" has been well-known, documented and a cause for concern for at least six years ... yet if you look at what's happening with Paulson's bailout plan, you'd think the administration just realized there were problems with the economy yesterday.

Feeling guilty about not following the economic system as it was milked to death by scheming fraudsters? I recently signed up for Nouriel Roubini's RGE monitor, as I thought his prognostications were right-on years ago. This is what I got (this is just one e-mail):

Greetings from RGE Monitor!

Check out all the great contributions that RGE has published this past week: Nouriel Roubini's Global EconoMonitor, RGE Analyst’s EconoMonitor, U.S. EconoMonitor, Emerging Markets Monitor, Global Macro EconoMonitor, Finance & Markets Monitor, Asia EconoMonitor, Latin America EconoMonitor and Europe EconoMonitor.

On Nouriel Roubini's Global EconoMonitor there are four ground-breaking pieces.

In the first, Nouriel explains that the lack of debt relief to distressed households is the reason why this financial crisis is becoming more severe and why the economic recession - with a sharp fall now in real consumption spending – is now worsening. One way of solving the problem is by creating HOME (Home Owners’ Mortgage Enterprise). In order to understand the idea behind HOME you should read: “We need a new HOLC - more than a new RTC or RFC- to provide massive debt relief to the household sector. We need to create the HOME (Home Owners’ Mortgage Enterprise).”

The second important piece by Nouriel Roubini discusses the demise of the shadow banking system. Among other things, he argues that the next steps of the collapse will be the run on the short term liabilities of hundreds of poor performing and highly leveraged hedge funds and the collapse of highly leveraged LBOs following the recent bust of the private equity bubble. Read: “The Shadow Banking System is Unravelling: Roubini Column in the Financial Times. Such demise confirmed by Morgan and Goldman now being converted into banks”

Nouriel’s third analysis poses an important question as to whether one or more systemically important funds could go belly up and lead to systemic shocks. In his view, even as no major player today is as leveraged as LTCM was in 1998, many of these funds are much larger than LTCM. So while until now the financial crisis has been concentrated among traditional banks, broker dealers and their off balance sheet structures (SIVs/conduits) one cannot rule out that some systemically important hedge funds may get into trouble with systemic consequences. Read: “The unraveling of the Shadow Banking System moves to hedge funds as Schmalpha replaces Alpha”.

Nouriel’s fourth piece defends the creation of HOME and offers a detailed explanation of the 10 steps in this HOME proposal to resolve this most severe financial crisis. Read: “HOME (Home Owners’ Mortgage Enterprise): A 10 Step Plan to Resolve the Financial Crisis”

Also don’t miss the replay of his most recent conference call, where he discusses the path that led us to this current crisis and the way out of it. Listen to: “Financial Crisis and Recession: The Worst is Ahead of Us”

On the RGE Analyst’s EconoMonitor Elisa Parisi-Capone details “The demise of the shadow banking system” Lehman’s default – a systemic event that forced a systemic solution – was the pivotal event that triggered a rapid succession of interventions.

Ayah el Said and Rachel Ziemba review the “Fallout of the Global Financial Turmoil in the Middle East” arguing that the region is not, if it ever was, immune from global trends with various home grown liquidity vulnerabilities exacerbated by global trends. Rachel Ziemba also reviews the recent performance of Singapore’s Investment Fund, GIC. See. “SWF Watch: Government of Singapore Investment Corporation (GIC)”

In U.S. Housing Retention Bill: How Effective in Stabilizing the U.S. Housing Market?, RGE Monitor analysts Arpitha Bykere and Christian Menegatti discuss the U.S. Government’s Housing Retention Bill to refinance mortgages of at-risk homeowners. They argue that this will largely be ineffective in containing the ongoing home price correction, the excess overhang of homes, and will have little impact on mortgage default and foreclosures.

On the U.S. EconoMonitor authors questioned the efficacy and fairness of the government's bailout measures. Tim Duy focused on a blind spot in the myopic bailout plan: "This program will actually reduce regulatory capital as losses are realized. Even after the bad assets are removed, the affected firms still need to be recapitalized, presumably via taxpayer infusions...Try as policymakers might, they cannot forever ignore the fact that we are not Japan; we do not have excess domestic savings to fund such a program...If the Bank of China continues to be a dominant financier of US excess, they have found a way to dominate the US in a way that could never have been achieved militarily. What is the alternative? A tax increase? Tell Americans six weeks before an election that they need to accept a lower standard of living?" See “Fed Watch: Friday Can’t Come Soon Enough“.

How to recapitalize and with whose money are two of the major points of contention in the bailout. Fabius Maximus raises the question of whether taxpayer funds will go into the pockets of insiders, as they did with the Resolution Trust Company and the Iraq War. Fabius Maximus lists these and other bailout concerns in “What do we know about the financial crisis? What are the key questions?”.

In “The Bailout of All Bailouts is a Bad Idea”, Robert Reich reminds policymakers "to pay adequate attention to the people whose wallets really keep the economy going, and who merit more help than the Wall Street tycoons whose carelessness and negligence have put it in such jeopardy."

In ”Financial Meltdown Reshaping Wall Street”, Elisa Parisi-Capone and Christian Menegatti frame the unknowns surrounding Lehman's bankruptcy and the fate of off-balance sheet toxic waste.

Also on the U.S. EconoMonitor this week:

What Wall Street Should Be Required to Do, to Get A Blank Check From Taxpayers by Robert Reich

The Fed giveth, and the Fed taketh away by Tim Price

CEO Clawback Provisions in the Bailout? by Barry Ritholtz

High priority report: a geopolitical sitrep on the financial crisis by Fabius Maximus

Why Paulson and Bernanke are only Partly Correct, and Why Main Street Needs More Direct Help by Robert Reich

The Allure (and Risk) of Silver Linings by James Picerno

Latest Bailout Plan Spin: Its a Money Maker! by Barry Ritholtz

A matched preferred stock plan for government assistance by Charles Calomiris

On the Emerging Markets Monitor Jelena Vukotic develops an interesting analysis of the geopolitical risks within the Eastern European region: “Recognition Practice and Geopolitical Risk in Eastern Europe: Georgia, Kosovo and Beyond”. Nirvikar Singh points out that “The current crisis in the US does not mark the end of financial capitalism, as some windy observers have claimed”. Finally, Steve Keen writes that “We've only just begun” , discussing the seriousness of the subprime mortgages issue and the potential risks to American households.

Also on the Emerging Markets Monitor:

Why You Should Hate the Treasury Bailout Proposal by Yves Smith

Morgan Stanley, Goldman to Become Banks by Yves Smith

This week in the Global Macro EconoMonitor Jeffrey Frankel argues that if Paulson’s $700 bn plan is going to provide capital to financial firms, the government should get a share in the banks’ ownership to prevent all the gains of the rescue plan accruing to people who made the mess in the first place. Read “An Emerging Consensus Against the Paulson Plan: Government Should Force Bank Capital Up, Not Just Socialize the Bad Loans”.

In “And Now the Great Depression”, Barry Eichengreen draws comparisons between the current financial crisis and the Great Depression and differentiates the causes and consequent policy responses of the ongoing crisis with those of the 1930s.

In “Falling Back to a New Redoubt”, Daniel Alpert argues that the government should focus on recapitalizing the banks and dealing with the continued decline in home prices and consequent mortgage default, and offers suggestions on how to make Paulson’s bailout plan more cost-effective.

In “FDIC Won't Run Out of Money, But WaMu May be Toast”, Chris Whalen reiterates that the deposit insurance fund is an accounting entry with the U.S. Treasury with the FDIC fund showing how much cash is contributed by the banks to support the deposit funds and the Treasury advancing the cash needed by FDIC to address bank failures and making the deposit guarantees.

Also on the Global Macro EconoMonitor this week:

Capitalism and Skepticism by Christopher Carroll

Ban on Short-Selling Will Hurt Rather Than Help Broker-Dealers by Yves Smith

Closing Comments September 19 2008 by John Jansen

Moral Hazard Misconception - Part 2 by Ricardo Caballero

A new sitrep, as we move into phase 3 of the financial crisis by Fabius Maximus

Fixing Housing & Finance: 30/20/10 Proposal by Barry Ritholtz

Essential steps to surviving the current crisis by Fabius Maximus

The Mystery of Capital Flows by Sebnem Kalemli-Ozcan

A vital but widely misunderstood aspect of our financial crisis by Fabius Maximus

Implications of Repricing of Dollar Denominated Assets by Menzie Chinn

What To Do (and Not To Do) In A Financial Panic by Christopher Carroll

A Desperate Struggle for Perspective...Againby James Picerno

A Simple Explanation of What Went Wrong by Barry Ritholtz

On the Finance & Markets Monitor, Daniel Gross proposes a put option format for calculating the value of outstanding RMBS contracts. Read:”‘No recourse’ and ‘put options’: Estimating the ‘fair value’ of US mortgage assets”.

According to Mark Thoma’s calculations, the value of subprime related securities may very well be close to zero. In “Who Should Pay for the Bailout?” The same author advocates that the government should implement a rescue plan as soon as possible, and that there should be a progressive tax system put in place, so that those who did not contribute to the credit crisis do not end up paying for it. The “Paulson bailout” by James Hamilton stipulates that modified capital standards and more stringent risk management procedures should be a requirement for any firm participating in the government bailout. In”Why Paulson is (maybe) right” Charles Wyplosz analyses the Paulson proposal and agrees with much of what has been done so far. However, the final judgment of the bailout’s efficacy will have to wait a few years, when the RTC has unloaded the currently toxic mortgage securities.

The idea that Paulson might be right is not a consensus. Indeed, for Luigi Zingales, the government should not bail out the financial industry. Read” Why Paulson is wrong”. For Zingales, the government should force the creditors to restructure, with part of the debt forgiven in exchange for an equity stake or warrants.

Then, in “Crack Addicts and Bubble Markets” Joseph Mason describes the current situation as an “’asymmetric information’ crisis”. He then proposes greater transparency as a solution, both for rating agencies and for accounting regulations. He also has qualms with the current bailout approach proposed by the Fed. In:” What is to be Done?: Interview with Bert Ely”, Chris Whalen conducts an in-depth interview with Bert Ely, a foremost banking expert and lobbyist, about the bailout and the overall state of the banking industry.

Also on the Finance & Markets Monitor this week:

The Unitary Federal Reserve - Crisis Choreography by London Banker

Some Thoughts For September 19 2008 by John Jansen

Terror Attack on US Financials? Details of SEC Short Ban by Barry Ritholtz

SEC Induced Mother-of-All Short Covering Rallies by Barry Ritholtz

When blatant government market manipulation won't help you... the Run on Morgan Stanley by Reggie Middleton

Ameribank: the latest FDIC bankruptcy takeover by Edward Harrison

"Non-Reviewable" - Sometimes there really ARE conspiracies by London Banker

News round-up: 21 Sep 2008 by Edward Harrison

October 18, 1930: NYT on Short Selling by Barry Ritholtz

America appoints a Magister Populi to deal with the financial crisis by Fabius Maximus

Opening Comments September 22 2008 by John Jansen

Opening Comments September 23 2008 by John Jansen

Wall Street, R.I.P. Now What? by James Picerno

Housing Prices: How Far to Go until Bottom? by Menzie Chinn

Banking Expert: Bailout Not Necessary, Industry Can Take Losses by Yves Smith

The Liquidation Trap by Thomas Palley

Main Street or Wall Street? by Mark Thoma

How SEC Regulatory Exemptions Helped Lead to Collapse by Barry Ritholtz

Illiquidity versus Insolvency by Paul Kedrosky

Libor-OIS spread at an all-time high by Edward Harrison

Opening Comments September 25 2008 by John Jansen

The Right Financial Fix by Laurence J. Kotlikoff

On the Asia EconoMonitor, Takeo Hoshi suggests that the government’s comprehensive plan is a welcome step but that it lacks any clear government approach on (near) insolvency of large financial institutions. Read “The Cure for the U.S. Financial System?” He also describes how the failure of Lehman produced serious problems in credit markets not only in the U.S. but also in Japan where the repo market collapsed. See “Lehman Shock and the Japanese Financial Markets”

In “Some Random Thoughts on the Chinese Yuan” Yin-Wong Cheung argues that pushing China to keep appreciating its currency, without other complementary policies in place, can bring more harm than benefits to the global economy.

Also on the Asia EconoMonitor:

Worrying about the banking system by Michael Pettis

Markets surge, but little has improved by Michael Pettis

Japan’s New Prime Minister and Economic Reform by Takeo Hoshi

On the Latin America EconoMonitor we have three outstanding contributions. The first two deal with different aspects of the Paulson plan and discuss how it might affect Latin countries. Read “A Short Note on the Banking and the Banking Crisis in the US” by Antonio Carlos Lemgruber and “The Paulson Plan, Money versus Debt, and the Reversal Auctions” by Luiz Cezar Fernandes. The talk of Latin markets this week has been broader than the Paulson plan and has included the fact that Argentina might offer the holdouts a proposal to pay the debt outstanding. If you want to get a better grip on the holdouts and Argentina, we recommend the latest piece by Eugenio Diaz Bonilla: Some Reflections on Argentina’s Debt Restructuring .

Also on the Latin America EconoMonitor:

Lack of Infrastructure Investment in Brazil: A Constraint on Economic Growth by Vitoria Saddi

On the Europe EconoMonitor Ulrich Fritsche and Georg Erber discuss the slowdown in German productivity. In their view, the extraordinary export performance and competitiveness of the German economy was mainly driven by massive wage restraints and not by productivity gains. Read “Labour productivity growth in good old Germany: is Germany falling further behind?”

As Russian equity markets plummeted in recent weeks, conspiracy theories circulated that Washington was egging on American financiers to punish Moscow for its actions in Georgia. Fabius Maximus argues that even though these rumors are most likely false, they signal that the possibility of financial warfare is on the minds of key people. Read: “Rumors of financial war: Russia vs. US”

Also on the Europe EconoMonitor, Daniel Gross and Stefano Micossi argue that $700bn nationalization of US financial institutions helped save so far many overleveraged Europe’s banks, whose total liabilities in some cases amount to or exceed their countries’ GDPs. For them the solutions for the large institutions can no longer be found at the national level and hence it seems apparent that the European Central Bank will need to be put in charge. Read “European banking on borrowed time”.

That's just from one site. I like to read prudentbear.com, Naked Capitalism, Charles Kingsley Michaelson's, "Someassemblyrequired", Atol, not to mention the NYT and other pubs....this is just impossible. No wonder we're a nation of addled idiots.

Thursday, September 25, 2008

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment